5 Ways to Cut Your GLP-1 Medication Costs in Half

Paying $1,000+ monthly for weight loss meds? Here are the actual strategies that work to slash your costs without sacrificing quality or safety.

Let me be blunt: GLP-1 medications are expensive as hell. I've watched friends pay $1,200 a month for Wegovy while others get the same results for $200. The difference isn't luck – it's knowing how to work the system.

After helping dozens of people navigate these costs (and dealing with my own sticker shock), I've learned which money-saving strategies actually work and which ones are just wishful thinking.

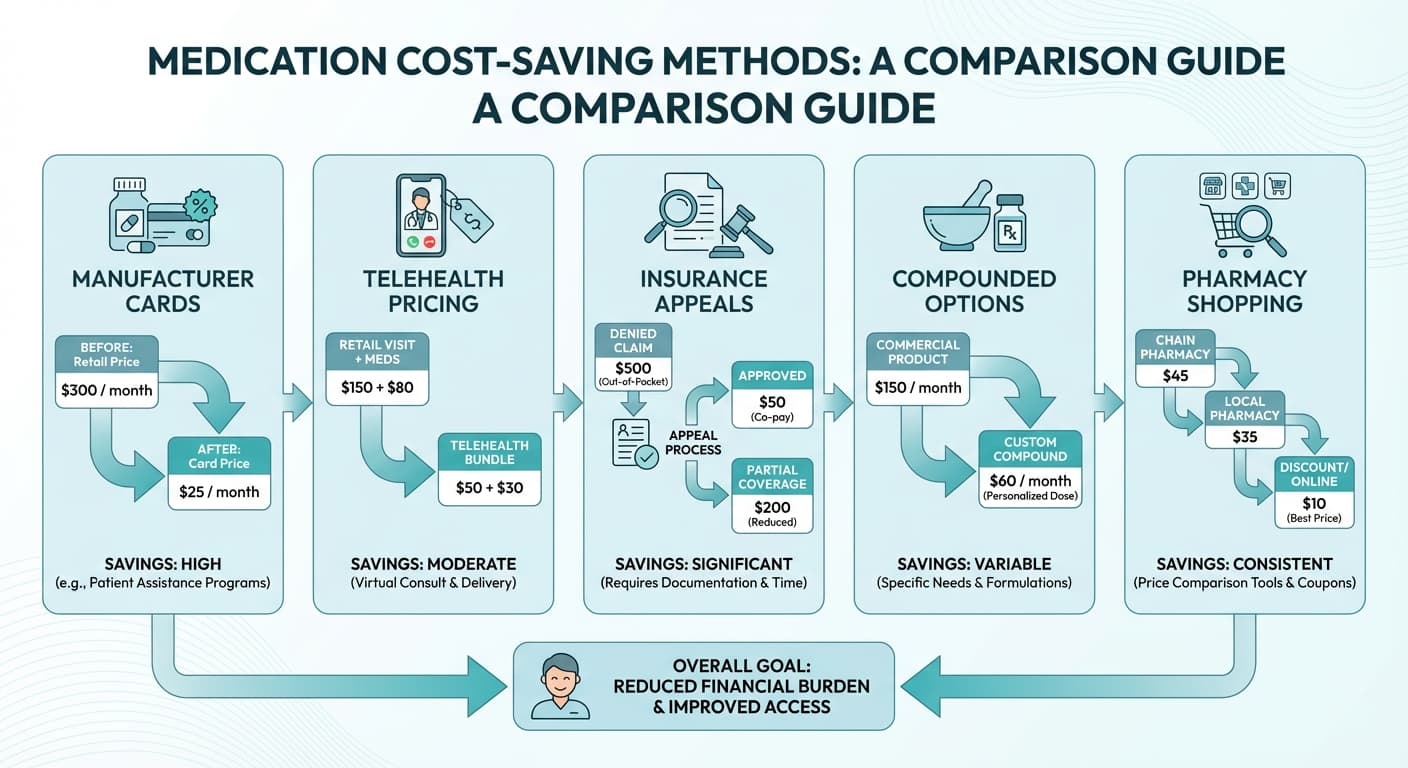

Start with Manufacturer Savings Programs

Here's what most people don't realize: the drug companies themselves offer the biggest discounts, but they're terrible at advertising them.

Novo Nordisk's savings card can drop your Wegovy copay to as low as $25 per month if you have commercial insurance. Eli Lilly offers similar deals for Zepbound – up to $550 off your monthly prescription. The catch? These programs have income limits and don't work with government insurance like Medicare or Medicaid.

Real talk: I've seen people assume they don't qualify without even checking. Takes five minutes to apply online, and the worst they can say is no.

The savings cards typically last 12-24 months, so you're not locked into full price forever. But read the fine print – some have annual caps that might leave you hanging if you hit the limit.

Telehealth Providers Can Beat Your Local Pharmacy

This one surprised me. Traditional pharmacies often charge whatever your insurance dictates, but telehealth companies negotiate their own rates.

Some telehealth providers bundle the medication cost into their monthly fee – you might pay $300-400 total instead of dealing with insurance copays that fluctuate. Others have relationships with specific pharmacies that offer better cash prices.

The honest answer? Pricing varies wildly between providers. I've seen the same dose of semaglutide range from $200 to $800 depending on where you go. Worth calling around before you commit.

What's tricky is that some telehealth companies are transparent about their all-in costs upfront, while others hit you with surprise fees after your consultation. Always ask for the total monthly cost including medication before you start.

Insurance Appeals Actually Work (If You Do Them Right)

Most insurance denials aren't final – they're just the first "no" in a negotiation process. But you've got to know how to play the game.

Your best shot is getting your doctor to document medical necessity beyond just weight loss. Sleep apnea, diabetes risk, joint problems – anything that shows this isn't cosmetic. Insurance companies are more likely to approve when there are multiple health benefits on the table.

The insurance approval process can take 30-90 days, so start early. And here's something nobody tells you: if your first appeal gets denied, file a second one. Different reviewers sometimes reach different conclusions.

One strategy that's worked for several people I know: ask your doctor to start with a lower-cost GLP-1 first (like older semaglutide formulations), then step up to newer options if insurance sees you're responding well.

Compounded Versions: The Wild West Option

Compounded GLP-1s can cost 60-80% less than brand names, but you're entering murky territory. These are custom-made versions from specialty pharmacies, not FDA-approved drugs.

The quality varies dramatically between compounding pharmacies. Some are excellent, others... not so much. You want a pharmacy that's FDA-registered, follows USP standards, and ideally has been around for years.

Here's what I've learned from people using compounded versions: the dosing can be less precise, and you might not get the same injection pens as brand names. Some come in vials that you draw up yourself – doable, but more complicated.

The savings can be substantial, but factor in that your insurance definitely won't cover compounded versions. You're paying cash, which means no copay assistance either.

Timing Your Prescription Fills

This sounds minor, but it can save you hundreds. If you're paying cash or have a high deductible, consider:

Buying 90-day supplies: Many pharmacies offer better per-dose pricing for larger quantities. Plus, some manufacturer coupons work better with 90-day fills.

Shopping around pharmacies: Cash prices vary by $200+ between different chains. Costco, even without membership for prescriptions, often beats CVS and Walgreens. Some independent pharmacies negotiate even better deals.

Using GoodRx strategically: The discounts aren't huge for GLP-1s, but every $50 helps. More importantly, GoodRx shows you which nearby pharmacies have the lowest cash prices.

What About International Options?

I get asked about ordering from other countries constantly. Yes, some people do it. No, I can't recommend it.

The legal grey area aside, you're gambling on medication that might not be stored properly during shipping, could be counterfeit, or might get seized by customs. The potential savings aren't worth the health risks.

Canadian pharmacies are slightly safer than other international options, but you're still dealing with medications that haven't gone through the same supply chain protections as US pharmacies.

Making the Math Work Long-Term

Here's the reality check: even with all these strategies, you're probably looking at $200-500 monthly. That's still a lot of money for most people.

Before you commit, think about your timeline. If you need to stay on these medications long-term for maintenance, factor that into your budget planning. Some people use the medication to lose weight initially, then transition to lifestyle changes, but that doesn't work for everyone.

The other thing to consider: as more GLP-1 options come to market, competition should drive prices down. The question is whether you want to wait or start now with current pricing.

Your Next Steps

Start with the manufacturer savings programs – they're the lowest-hanging fruit. Then compare telehealth pricing against your local options. If insurance is your plan, get your doctor involved early in building a strong case for medical necessity.

Don't try to save money by skipping doses or sharing prescriptions. These medications work best with consistent dosing, and messing with that defeats the purpose of spending the money in the first place.

The bottom line: there are legitimate ways to cut your costs significantly, but it takes some legwork upfront. Given what you're potentially spending annually, it's worth investing a few hours to research your options.