The Real Cost Breakdown: Brand vs Compounded GLP-1s

Compounded semaglutide can cost $300 less per month than Wegovy, but there's more to consider than just the price tag.

The Numbers Don't Lie: What You're Actually Paying

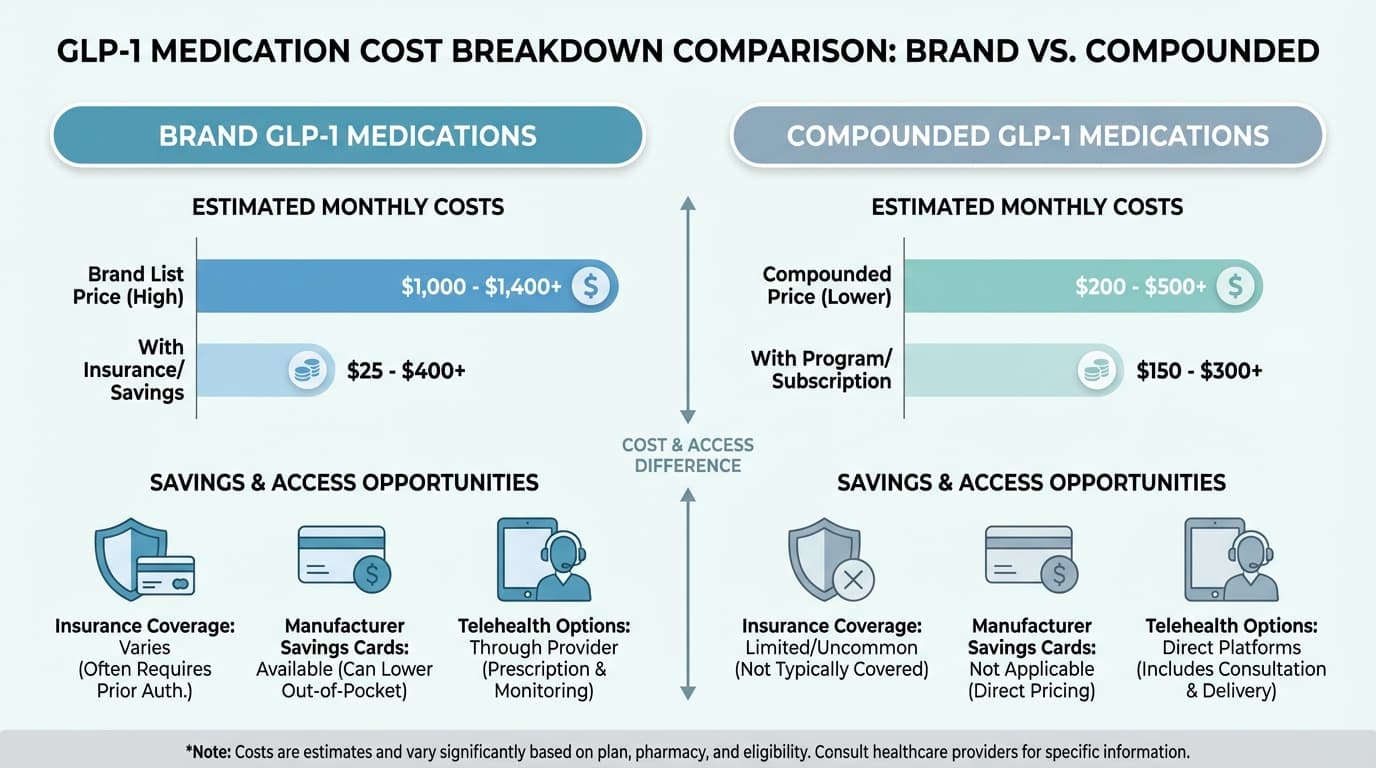

Let's cut straight to what matters most - your wallet. Brand-name Wegovy runs about $1,349 per month without insurance. Compounded semaglutide? You're looking at $200-400 monthly through most telehealth providers. That's a difference that could literally pay your car payment.

But here's what most people don't realize: the cheapest option isn't always the smartest choice. After spending months researching this stuff and talking to people who've tried both routes, I've learned there are hidden costs and benefits that nobody talks about upfront.

Brand Names: Expensive but Predictable

When you pick up Wegovy, Ozempic, Mounjaro, or Zepbound from your pharmacy, you're paying for consistency. Each dose contains exactly what the label says, manufactured in FDA-approved facilities with strict quality controls.

The real advantage? Insurance coverage. Most major insurers have some coverage for brand medications, especially if your doctor can prove medical necessity. Your copay might still be $25-100 monthly instead of the full retail price.

Manufacturer savings cards are where things get interesting. Novo Nordisk offers up to $200 off Wegovy monthly for qualifying patients. Eli Lilly's program can reduce Mounjaro costs to as low as $25 per month for some people. These aren't forever deals - they typically last 12-24 months - but they can make brand medications surprisingly affordable if you qualify.

The catch? You usually can't combine manufacturer savings with government insurance like Medicare or Medicaid. It's private insurance or pay full price.

Compounded Medications: The Wild West of Savings

Compounded versions contain the same active ingredient as brand medications, but they're mixed by specialized pharmacies rather than big pharmaceutical companies. The FDA doesn't pre-approve these formulations, which keeps costs way down but adds some uncertainty.

Real talk: I've heard from people who've had great experiences with compounded semaglutide and others who've struggled with inconsistent effects between batches. The active ingredient is the same, but things like absorption rates can vary based on how it's formulated.

Most telehealth providers offering compounded options charge $200-400 monthly, including the medication and provider consultations. Some popular platforms price it around $300 per month, while others start as low as $179. The convenience factor is huge - everything ships to your door, and you don't need to navigate insurance approval processes.

Telehealth Provider Shopping: It Pays to Compare

Not all telehealth providers price their services the same way. Some charge separately for consultations ($50-100) and medication ($200-300). Others bundle everything into one monthly fee.

What to look for when comparing providers:- Total monthly cost including consultations- How often you need provider check-ins- What happens if you need to adjust doses- Shipping costs and frequency- Whether they offer both semaglutide and tirzepatide options

Some providers offer discounts for longer commitments, like $50 off monthly if you pay for three months upfront. Others have referral programs or seasonal promotions. It's worth checking a few different platforms before committing.

Insurance Strategies That Actually Work

Your insurance approach depends entirely on whether you're going brand or compounded. For brand medications, prior authorization is your biggest hurdle. Your doctor needs to document that you've tried other weight loss methods and that you meet specific BMI or health criteria.

The honest answer? Getting insurance approval can take weeks or even months. But once you're approved, your monthly costs drop dramatically. I know people paying $25 monthly for Mounjaro with good insurance coverage.

For compounded medications, insurance typically won't cover anything. You're paying out of pocket, but at least you know exactly what to budget each month.

One strategy that works: start with a compounded version while working on insurance approval for brand medication. This way, you can begin treatment immediately instead of waiting months for prior authorization.

Hidden Costs Nobody Mentions

With brand medications, pharmacy pickup fees, missed appointment costs for insurance requirements, and potential copays for required lab work add up. Some insurance plans require quarterly check-ins with specialists, which means more copays.

Compounded medications have their own hidden expenses. If you need to switch providers because of supply issues or quality concerns, you're starting over with new consultation fees. Some people end up paying for multiple providers while finding one that works reliably.

Shipping costs vary wildly between telehealth providers. A few include overnight shipping in their pricing, while others charge $20-40 extra for faster delivery. When you're dealing with refrigerated medications, shipping delays can be expensive.

Making the Choice: What Works for Your Situation

If you have decent insurance and don't mind navigating prior authorization paperwork, brand medications often end up being the better financial choice long-term. The manufacturer savings programs can make your first year or two very affordable.

Compounded versions make sense if you want to start immediately, have insurance that definitely won't cover weight loss medications, or prefer the convenience of telehealth management. Just factor in the possibility that you might need to switch providers if quality or availability becomes an issue.

Here's the thing: your financial strategy might change over time. Many people start with compounded medications for quick access, then switch to brand versions once insurance approval comes through. Others find a telehealth provider they love and stick with compounded versions indefinitely.

Timing Your Financial Strategy

End-of-year timing matters more than most people realize. If you're close to meeting your insurance deductible, that's often the best time to push for brand medication approval. Once you've hit your deductible, your medication costs drop significantly.

Manufacturer savings programs typically reset in January, so you get a fresh allocation of discounts. Some people time their treatment start to maximize these benefits.

For compounded medications, some telehealth providers offer better pricing during slower months. It's worth asking about promotional pricing, especially if you're willing to commit to several months upfront.

The bottom line? There's no universally "right" choice between brand and compounded medications. Your best option depends on your insurance situation, budget, tolerance for uncertainty, and how quickly you want to start treatment. What matters most is finding an approach that you can afford consistently, because stopping and starting these medications rarely works well.

Take time to research your specific insurance coverage, compare multiple telehealth providers if you're considering compounded options, and don't be afraid to ask providers directly about savings programs or promotional pricing. The money you save on research upfront can add up to hundreds of dollars monthly once you start treatment.